Direct Cost

Definition

- identify direct costs specifically and exclusively with a given cost object in an economically feasible way

Characteristics

- physically identify the amount of the cost that relates exclusively to a particular cost object.

tracing the direct cost to the cost object

Indirect Cost

Definition

- Indirect costs cannot be identified specifically and exclusively with a given cost objective in an economically feasible way.

- Assign indirect costs to cost objects

Examples

- facilities rental costs, depreciation on equipment, and many staff salaries

Cost Allcation

Definition

- Cost allocation assigns indirect costs to cost objects, in proportion to the cost object’s use of a particular cost-allocation base.

- base is some measure of input or output that determines the amount of cost to be allocated to a particular cost object.

- 通常就是cost driver

- Why need?

- strategic decision

- operational control

- external reporting

- pruposes:

- predict economic effects

- setting the optimal product and customer mix, pricing policy, chose value-chain function to develop as core competencies

- predict the economic benefits and costs of process improvement efforts

- provide desired motivation and feedback for performance evaluation

- compute income and asset valuations for financial accounting

- justify costs or obtain reimbursement

理想情况下,成本分配应该同时满足四个需求

但是,成本分配通常也是一个迷惑和冲突的主要来源

分配 固定成本 经常造成最大的问题

管理者应该 识别哪个目的是最重要的 “Different cost for different purposes”

- predict economic effects

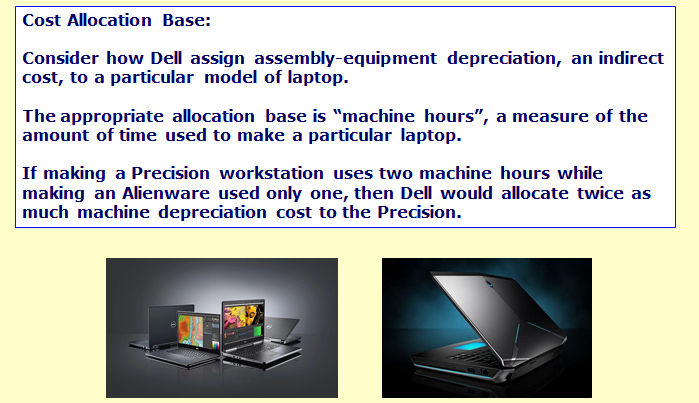

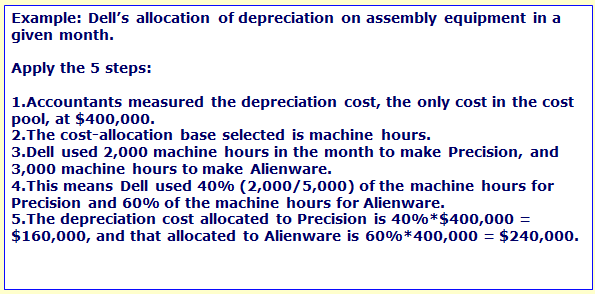

Example

- Dell:

Selection

- base should be a measure of how much of the particular cost is caused by the cost objective

- At most circumstances: most allocation bases are cost drivers

Method of Allocation Costs

- direct costs: tracing

- indirect costs: allocate using a cost-allocation base

Cost Pool

Definition

- Individual costs allocated to cost objects using a single cost-allocation base.

Steps

- Accumulate indirect costs for a period of time

- select an allocation base

- 计量每一个product使用了多少cost-allocation base

- 按照数量的比例分配cost pool中的成本到单个产品

Examples

Unallocated Cost

- might include R&D, legal design, accounting…

- just leave them alone

Examples

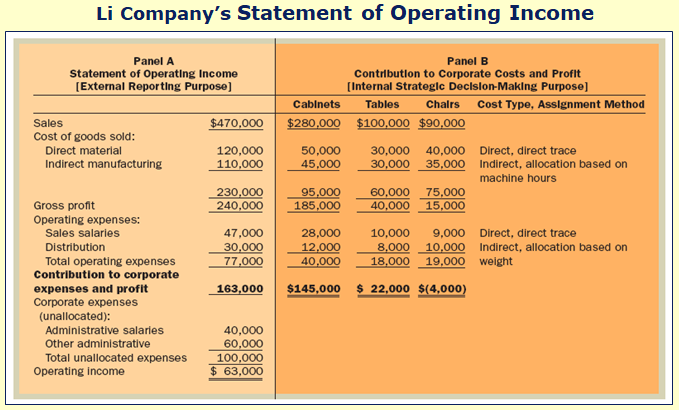

For External Reporting Purposes

- 成本会计系统的目的之一就是提供存货的度量和COGS的度量

- Four Attributes

- Manufacturing costs

- Product versus period costs

- Costs on the balance sheet

- Costs on the income statement

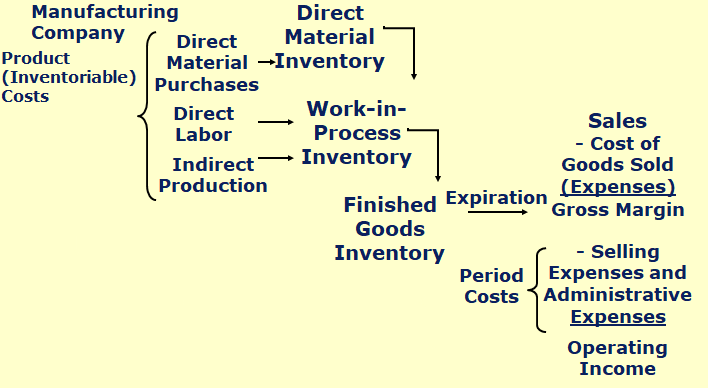

Manufacturing Costs

- Direct-material costs

- Direct-labor costs

- Indirect production costs(Overhead)

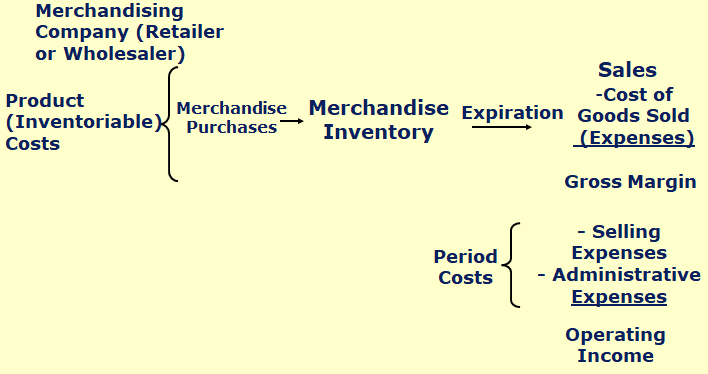

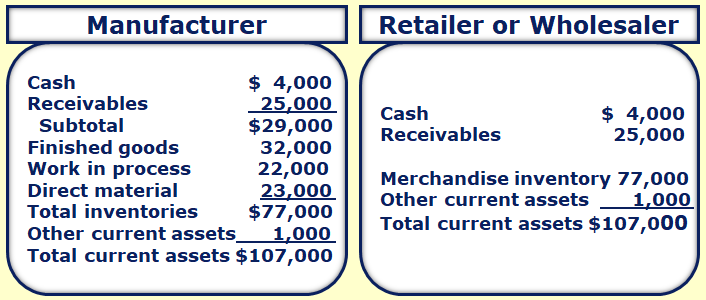

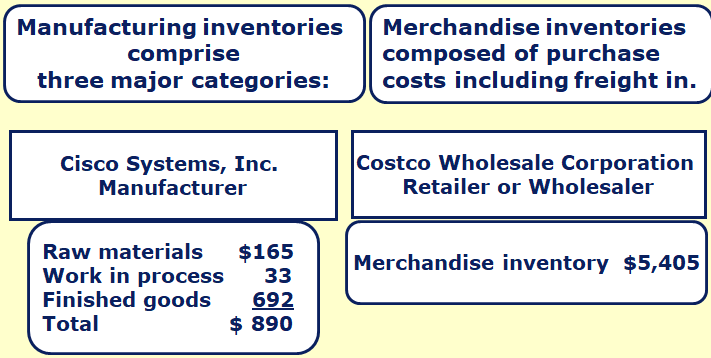

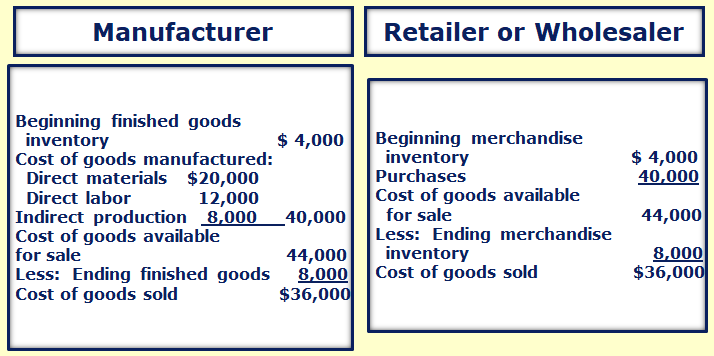

Merchandising Company

Manufacturing Company

Comparing

- Current Assets

- Inventory

- COGS

Activity-Based Management

Definition

- Using the output of an activity-based cost accounting system to aid strategic decision making and to improve operational control

- A value-added cost should be included

- Nonvalue-added costs can be eliminated without affecting a product’s value to the customer

Benchmarking

- continuous process of comparing products, services and activities to the best industry standards

Benefits of ABC

- set an optimal product mix

- estimate profit margins of new products

- determine consumption of shared resources

- keep pace with new product techniques

- keep pace with technological changes

- decrease costs associated with bad decisions

- take advantage of reduced cost of ABC systems due to computer technology

To design an ABC system

- Determine the key components of the cost accounting system

- cost objectives(成本对象:比如commercial和residential顾客 )

- key activities(主要要从事哪些业务活动,形成activity dictionary)

- resources (每个activity需要消耗的资源,以及企业本身的资源)

- related cost drivers(成本和行为之间的因果关系,把resource和activity联系起来的,把activity和objective联系起来的成本动因)

- Determine relationships among cost objectives, activities, and resources

- Collect relevant data concerning costs and the physical flow of the cost-driver units among resources and activities

- calculate and interpret the new activity-based information

- determine the traceable costs for each of the activity cost pools

- Determine the activity-based cost for account for each customer class.

Design of a Traditional Costing System

- 将间接成本只按一个cost driver 分配