When you have finished studying this chapter, you should be able to:

- Explain how activity cost drivers affect cost behavior.

- Show how changes in cost driver levels affect variable and fixed costs.

- Calculate break-even sales volume in total dollars and total units.

- Create a cost-volume-profit graph and understand the assumptions behind it.

- Calculate sales volume in total dollars and total units to reach a target profit.

- Differentiate between contribution margin and gross margin.

- Explain the effects of sales mix on profits (Appendix 2A).

- Compute cost-volume-profit relationships on an after-tax basis (Appendix 2B).

Cost Drivers and Cost Behavior

Definitions

Cost drivers are measures of activities that require the use of resources and thereby cause costs.

Cost behavior is how the activities of an organization affect its costs.

Examples

Value Chain Function

Research and development

Salaries of sales personnel, costs of market surveys

Salaries of product and process engineers

Design of products, services, and processes

- Salaries of product and process engineers

- Cost of computer-aided design equipment used to develop prototype of product for testing

Production

Labor wages

Supervisory salaries

Maintenance wages

Depreciation of plant and machinery, supplies

Energy cost

Marketing

Cost of advertisements

Salaries of marketing personnel, travel costs, entertainment costs

Distribution

Wages of shipping personnel

Transportation costs including depreciation of vehicles and fuel

Customer service

Salaries of service personnel

Costs of supplies, travel

Example of Cost Drivers:

Number of new product proposals

Complexity of proposed products

Number of engineering hours

Number of distinct parts per product

Labor hours

Number of people supervised

Number of mechanic hours

Number of machine hours

Kilowatt hours

Number of advertisements

Sales dollars

Labor hours

Weight of items delivered

Hours spent servicing products

Number of service calls

Relevant Range

Definition

- The relevant range is the limit of cost-driver activity level within which a specific relationship between costs and the cost driver is valid.

- Even within the relevant range, a fixed cost remains fixed only over a given period of time — usually the budget period.

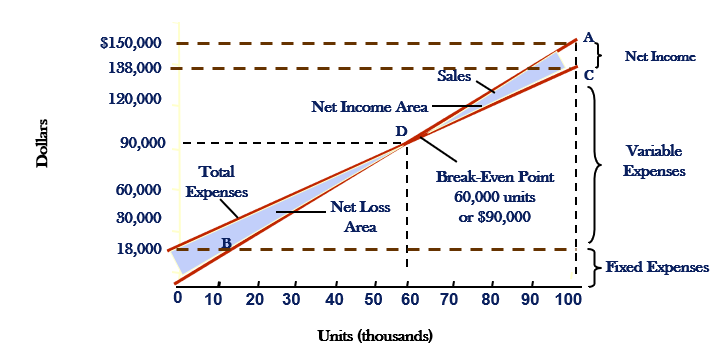

CVP Scenario

- The study of the effects of output volume on revenue(sales), expenses(costs), and net income(net profit).

Break-Even Point

- the level of sales at which revenue equals expenses and net income is zero.

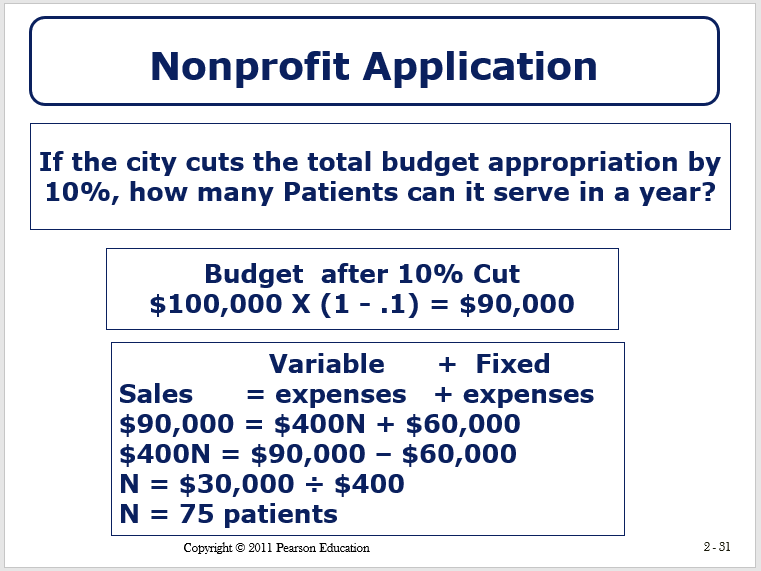

Target Net Profit

- Formula: $Target Sales Volume In Units = \frac{Fixed expenses + Target net income}{Contribution margin per unit}$

- contribution margin ratio = unit contribution / selling price

Sales volume in dollars = fixed expenses+target net income/contribution margin ratio

An example:

Margin of Safety

- How far sales can fall before losses occur and is the difference between the level of planned sales and the break-even point.

- margin of safety in units = planned unit sales - break-even unit sales

Operating Leverage

- A firm’s ratio of fixed costs to variable costs