Audit procedure - risk based audit approach

The purpose of external audit engagements

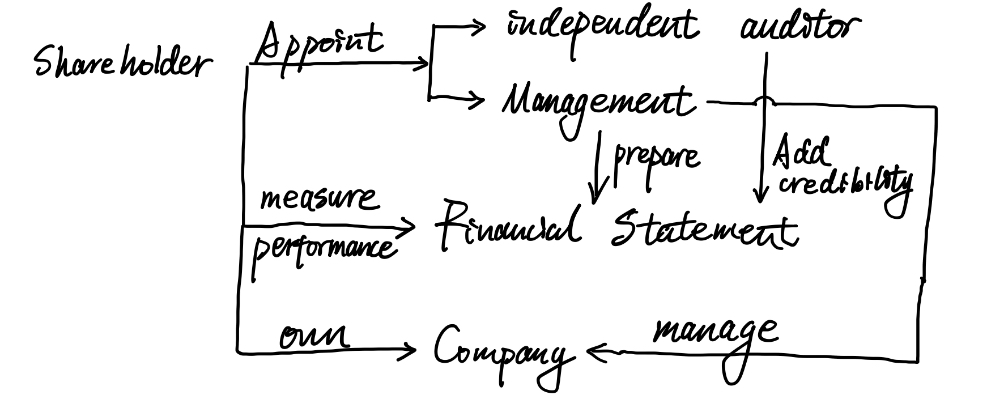

The Objective of external audit

- 审计财报的目的:

- Enable the auditor to express an independent opinion on whether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework.

- That opinion: whether the financial statements are presented fairly, in all material respect, or give a true and fair view in accordance with the framework. Based on ISAs and other relevant ethical requirements.

- By-products: Like advice to the directors on how to run the business. But its objective is solely to report to the shareholders.

- A flow chart:

Accountability, stewardship and agency

- The reason why audit provides assurance to the shareholders and other stakeholders of a company on the financial statements because it is independent and impartial.

Accountability:

- The quality or state of being accountable; that is, being required or expected to justify actions and decisions. It suggests an obligation or willingness to accept responsibility for one’s action.

Stewardship:

- Stewardship refers to the duties and obligations of a person who manages another person’s property.

Agency:

- Agents are people employed or used to provide a particular service. In the case of a company, the people being used to provide the service of managing the business also have the second role of trying to maximize their personal wealth in their own right.

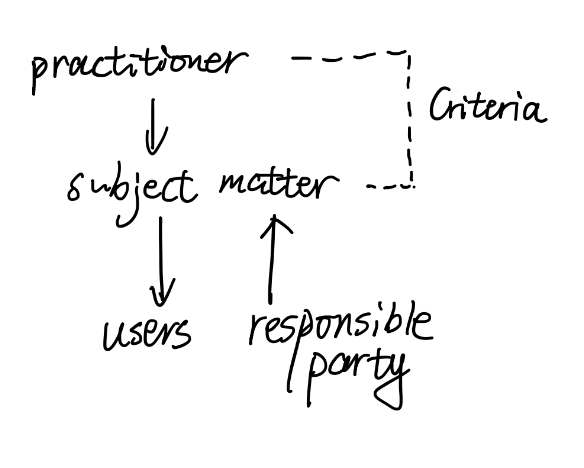

Assurance provision:

one in which a practitioner expresses a conclusion designed to enhance the degree of confidence of the intended users other than the responsible party about the subject matter information (that is, the outcome of the evaluation or measurement of a subject matter against criteria.)

Elements of an assurance:

| engagement | CREST |

|---|---|

| suitable criteria | criteria |

| a subject matter | report |

| evidence | evidence |

| a subject matter | subject matter |

| a three party relationship | three party relationship |

Responsibility of external auditor:

- obtain reasonable assurance about whether the financial statement as a whole are free from material misstatement whether due to fraud or error

- reasonable assurance:

- high level of assurance: obtained when the auditor has obtained sufficient appropriate evidence to reduce audit risk.

- audit risk: the risk that the auditor expresses an inappropriate opinion when the financial statements are materially misstated to an acceptably low level. (审计师发表了不合适观点,当财报有严重错误)

- not an absolute level of assurance: inherent(固有的) limitations of an audit which result in most of the audit evidence on which the auditor draws conclusions and bases the auditor’s opinion being persuasive rather than conclusion.

Types of assurance services

Statutory Audits - like external auditor

Non-Statutory Audits - like internal auditor

Advantages:

- means of settling accounts (结账方便)

- accounts may be more acceptable to taxation authority

- may facilitate the sale of the business, or negotiation of a loan

- useful for a sleeping partner

Internal auditors

- often benefit external auditors

- employed as part of an organization’s system of controls. Responsibilities are determined by management and may be wide-ranging.

- an appraisal or monitoring activity established or provided as a service to the entity, including evaluating and monitoring the adequacy and effectiveness of internal control

Types

- value for money audits(economy, efficiency and effectiveness)

- information technology audit

- best value audits

- financial, operational and procurement audits

- review engagement: 季度审计, give an opinion on whether anything has come to his attention that would mean the FS were not properly prepared/true and fair, on the basis of procedures which would not constitute an audit.

Assurance and reports

Auditor’s responsibility

auditors report on company financial statements is expressed in terms of truth and fairness.

- factual

- free from bias

- reflect the commercial substance of the business’s transactions

give an opinion on the fair presentation, or truth and fairness, of financial statement

- True: factual, conforms with required standards and law

- Fair: clear, impartial, free from discrimination and bias, should reflect commercial substance of transactions

- not an opinion of absolute correctness

Levels of assurance

| types | form of conclusion | example |

|---|---|---|

| reasonable | positive | statutory external audit |

| limited | negative | forecast review of interim financial statements |

- reasonable assurane:

- require a lot of detailed work

- a high level of assurance

- provide assurance on directors’ assertion that the financial statements give a true and fair view

- must:

- assess risk

- plan audit procedures

- conduct audit procedures

- assess results

- express an opinion

Review engagement

- 判断依据:

- Nature of subject matter: future or historic?

- The extent to which the audit procedures carried out